Price In The Economy Explained for SHS 1 Economics (Semester 2, Week 4)

Every purchase we make involves a price. Whether buying food, clothing, transportation, or electronic devices, price influences our decisions and plays a vital role in the economy.

What You Will Learn

- The meaning of price

- How prices are determined

- The relationship between price, demand, and supply

- The role of price in economic decision-making

- The importance of price in resource allocation

Main Explanation

Price is the monetary value or amount of money assigned to a good, service, resource, or asset in the market. It represents the cost that buyers must pay to acquire goods and services from sellers. Price is one of the most important tools used in economic systems to coordinate production and consumption activities.

Prices are determined through the interaction of demand and supply. When demand for a product increases while supply remains limited, prices tend to rise. On the other hand, when demand is low relative to supply, prices tend to fall. The interaction between demand and supply eventually leads to an equilibrium price, where quantity demanded equals quantity supplied.

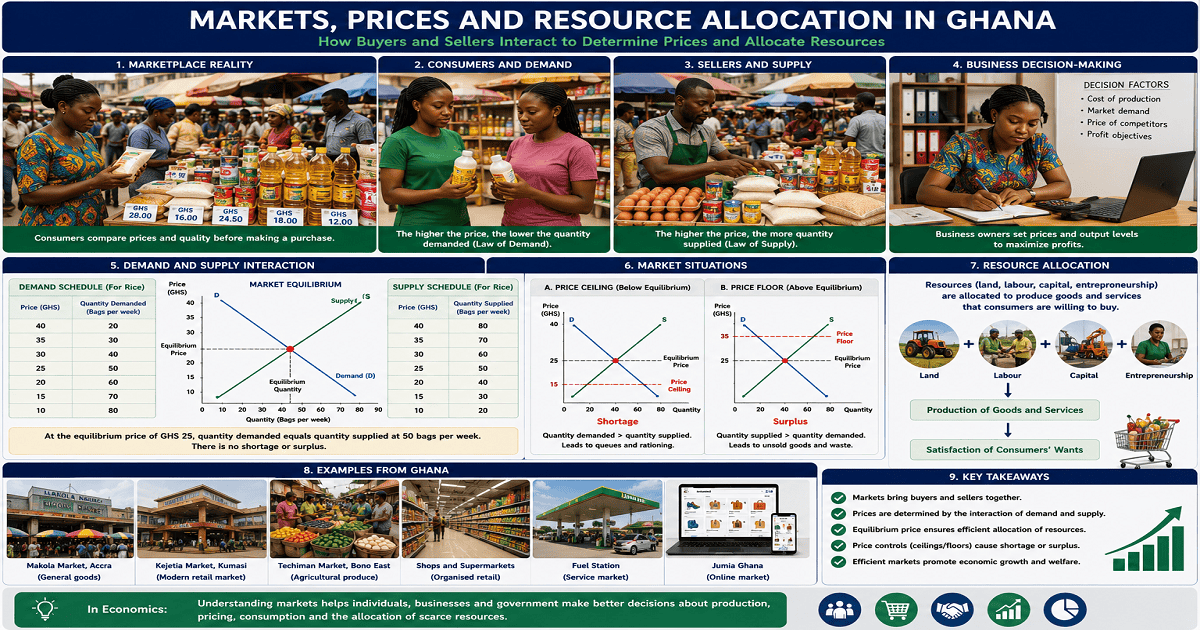

Price serves as a communication tool in the market. It provides information to producers about what consumers want and informs consumers about the value and availability of products. Through this process, resources are allocated to sectors where they are most needed.

Price also plays an important role in financial markets. Investors use prices to evaluate assets such as stocks, real estate, and commodities. Changes in prices often influence investment decisions and expectations about future market conditions.

Consumers rely on prices when making purchasing decisions. For example, when choosing among different brands of rice, consumers often compare prices alongside quality and personal preferences. The rice price tags illustrated in the source material demonstrate how prices can influence consumer choices and spending patterns.

For producers, rising prices may indicate increased demand or scarcity, encouraging them to increase production. Falling prices may signal lower demand and cause producers to reduce output.

Roles Of Price In The Economy

| Role | Explanation | Benefit |

|---|---|---|

| Resource Allocation | Directs resources to productive uses | Improves efficiency |

| Decision-Making | Guides buyers and sellers | Supports informed choices |

| Value Measurement | Indicates the worth of goods and services | Facilitates trade |

| Production Guidance | Signals changes in demand and supply | Influences output decisions |

Demand, Supply, And Price

| Situation | Expected Price Movement | Reason |

|---|---|---|

| Demand increases while supply remains low | Price rises | Greater competition among buyers |

| Supply increases while demand remains low | Price falls | Excess products in the market |

| Demand equals supply | Stable price | Market equilibrium achieved |

Worked Examples

Example 1

Scenario: A popular smartphone experiences a sudden increase in demand while production remains unchanged.

Explanation: Because more consumers want the product but supply remains limited, the market price is likely to increase until equilibrium is restored.

Example 2

Scenario: A consumer compares three brands of rice with different prices before making a purchase.

Explanation: Price influences the consumer’s decision because it affects affordability and perceived value. The buyer may choose the option that best fits their budget and preferences.

Why This Topic Matters

Understanding price helps learners appreciate how markets function and how economic decisions are made. Prices affect production, consumption, investment, and resource allocation. Knowledge of price determination enables individuals to make informed choices as consumers, producers, and future investors.

Quick Practice

- Define price.

- Explain the relationship between demand, supply, and price.

- State one way price affects consumer decisions.

Summary

Price is the monetary value assigned to goods, services, resources, and assets. It is determined by the interaction of demand and supply and plays a central role in market coordination, resource allocation, production decisions, and consumer behaviour. Through price signals, economies are able to allocate resources efficiently and respond to changing market conditions.

Access NaCCA-aligned Support Packs

Download your structured NaCCA-aligned Teacher Support Pack and Student Learning Pack, designed for clarity, practicality, and reliable teaching and learning.