Price In The Economy

Introduction

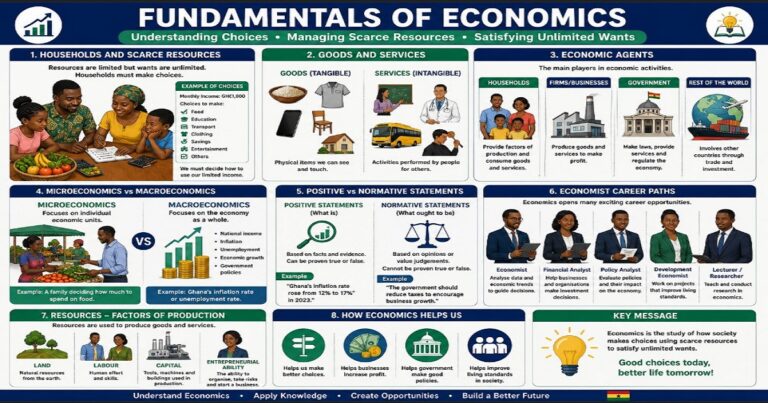

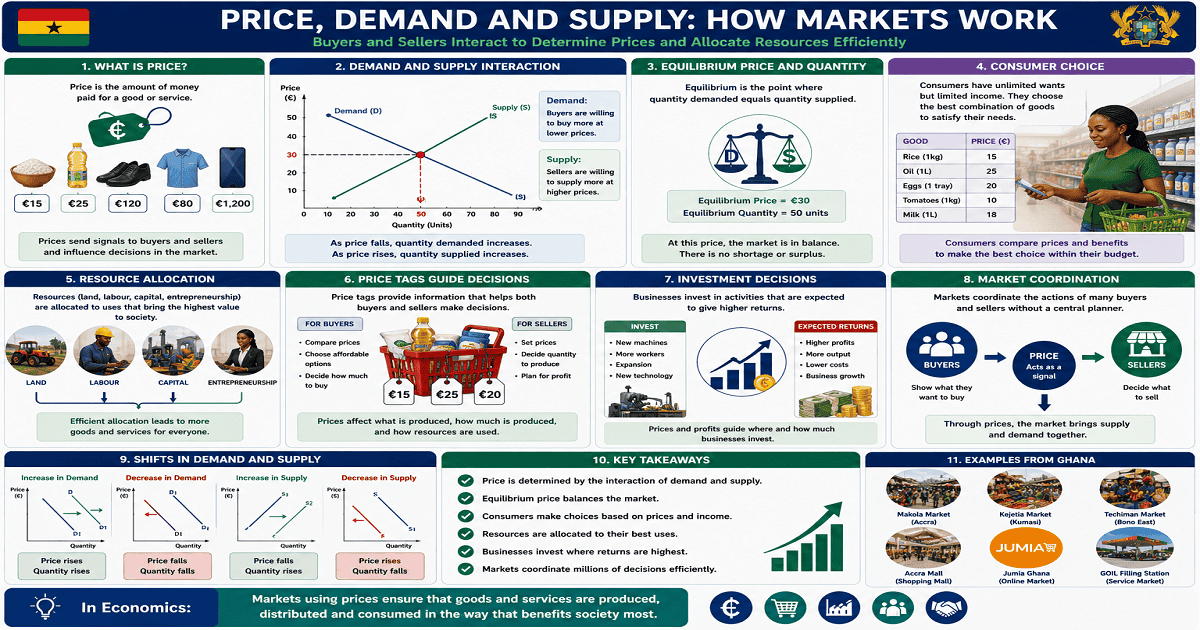

Price is one of the most important concepts in economics because it influences the decisions of consumers, producers, investors, and governments. It serves as a signal that helps determine what goods and services should be produced, how resources should be allocated, and how markets operate. Through the interaction of demand and supply, prices help coordinate economic activities and facilitate the exchange of goods and services.

Key Concepts

- Price: The monetary value, amount of money, or rate assigned to a good, service, resource, or asset in the market.

- Demand: The willingness and ability of consumers to purchase goods and services at different prices.

- Supply: The willingness and ability of producers to offer goods and services for sale.

- Equilibrium Price: The price at which quantity demanded equals quantity supplied.

- Resource Allocation: The distribution of resources to different sectors of the economy.

- Market Coordination: The process through which buyers and sellers interact to determine prices and quantities.

- Consumer Choice: Decisions made by buyers regarding which goods and services to purchase.

- Asset Price: The value assigned to assets such as stocks, real estate, and commodities.

Explanation

Price is the monetary value or amount of money assigned to a good, service, resource, or asset in the market. It represents the amount that a buyer must pay to obtain a product or service from a seller. Prices are fundamental to economic systems because they influence production, consumption, and investment decisions.

Prices are determined through the interaction of demand and supply. When demand for a product is high and supply is limited, prices tend to increase. Conversely, when demand is low relative to supply, prices tend to decrease. This interaction continues until an equilibrium price is reached, where the quantity demanded equals the quantity supplied.

Price plays an important role in facilitating the exchange of goods and services between buyers and sellers. In a market economy, prices communicate information about the value of products and services, helping both consumers and producers make informed decisions. Through price signals, resources are allocated efficiently to sectors where demand is highest.

Prices are also important in financial markets. They are used to determine the value of assets such as stocks, real estate, and commodities. Investors use current and expected future prices to make investment decisions. When prices rise, it often signals greater demand or scarcity, encouraging producers to increase production and allocate more resources to that sector.

Price influences consumer behaviour. Consumers often compare prices before making purchases, while producers consider prices when deciding how much to produce. The image in the source material showing different bags of rice with price tags illustrates how prices can influence consumer choices among available alternatives.

Functions Of Price In The Economy

| Function | Description | Economic Importance |

|---|---|---|

| Resource Allocation | Directs resources to areas of higher demand | Improves efficiency |

| Market Coordination | Links buyers and sellers | Facilitates exchange |

| Decision-Making | Guides consumer and producer choices | Supports economic planning |

| Value Measurement | Determines the worth of goods and assets | Supports transactions |

| Production Signal | Indicates scarcity or abundance | Influences production levels |

How Demand And Supply Affect Price

| Market Condition | Demand | Supply | Price Movement |

|---|---|---|---|

| High Demand, Limited Supply | High | Low | Price rises |

| Low Demand, High Supply | Low | High | Price falls |

| Demand Equals Supply | Balanced | Balanced | Equilibrium price |

Applications Of Price

| Area | Application | Outcome |

|---|---|---|

| Consumer Decisions | Comparing product prices | Better purchasing choices |

| Business Decisions | Determining production levels | Efficient resource use |

| Investment Decisions | Evaluating asset values | Informed investments |

| Market Analysis | Studying price trends | Improved planning |

Examples

Example 1

Problem: Explain what happens to the price of a product when demand increases but supply remains limited.

- Identify the change in demand.

- Examine the level of supply.

- Determine the effect on price.

Final Answer: The price rises because more consumers are competing for a limited quantity of the product.

Example 2

Problem: Explain how price influences consumer choice when purchasing rice.

- Compare the prices of different brands.

- Consider available income.

- Select the most preferred option.

Final Answer: Consumers often choose products that provide the best value within their budget, making price an important factor in purchasing decisions.

Application and Activities

- Compare the prices of similar products in local shops.

- Discuss how demand and supply influence prices in your community.

- Observe how price differences affect consumer choices.

- Identify products whose prices have changed recently and explain possible reasons.

Practice Questions

- Define price.

- Explain how demand and supply determine price.

- Discuss two ways in which price influences consumer decision-making.

Summary

Price is the monetary value assigned to goods, services, resources, or assets in the market. It is determined through the interaction of demand and supply and plays a crucial role in resource allocation, market coordination, production decisions, consumer choices, and investment activities. Prices communicate information about scarcity and value, helping economies function efficiently and enabling buyers and sellers to make informed decisions.

Access NaCCA-aligned Support Packs

Download your structured NaCCA-aligned Teacher Support Pack and Student Learning Pack, designed for clarity, practicality, and reliable teaching and learning.