Principles, Types And Classification Of Taxation Explained for SHS 2 Economics (Semester 2, Week 8)

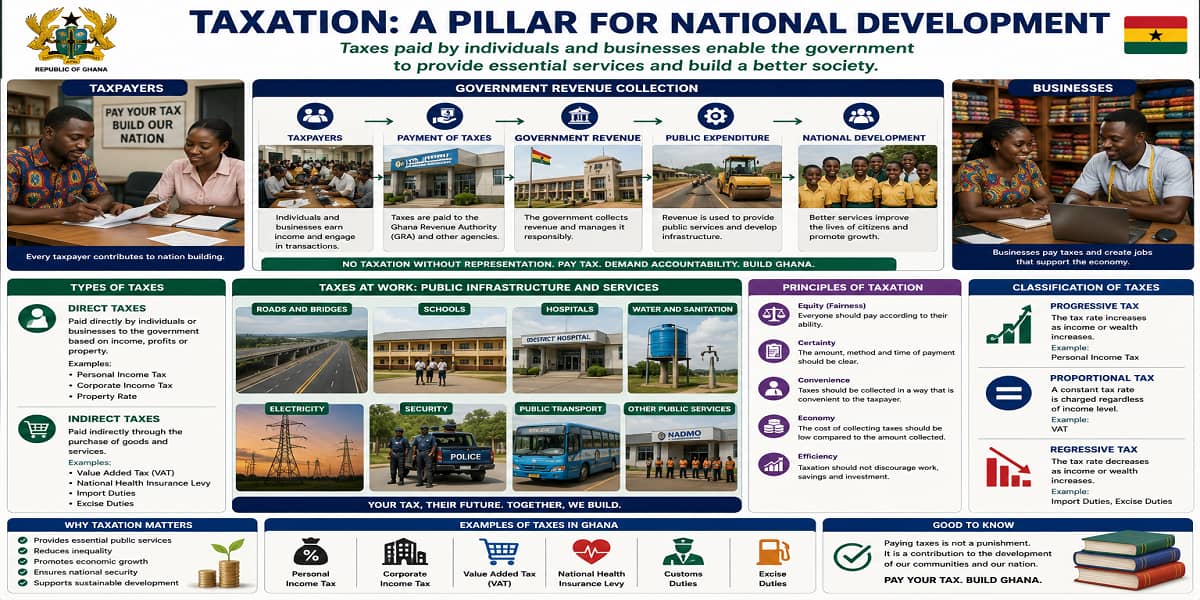

Governments require revenue to provide essential services such as education, healthcare, roads, and security. Taxation serves as one of the major sources of this revenue and plays an important role in economic development.

What You Will Learn

- The meaning of taxation

- The principles of taxation

- The types of taxes

- The different classifications of taxes

- Examples of taxes and their applications

Main Explanation

Taxation is the process through which governments or authorised agencies impose levies on individuals, businesses, and other entities. The main purpose of taxation is to generate revenue needed to finance public goods and services such as roads, healthcare, education, defence, and social welfare programmes. Taxation also contributes to economic stability and resource distribution.

The tax system is guided by several principles. Equity ensures fairness in tax payments. Efficiency seeks to minimise distortions in economic activities. Simplicity makes tax systems easy to understand, while certainty enables taxpayers to know their obligations. Convenience allows taxes to be paid in suitable ways, and revenue sufficiency ensures that government obtains adequate funds for expenditure.

Taxes are divided into two major categories: direct and indirect taxes. Direct taxes are imposed directly on individuals and businesses, whereas indirect taxes are levied on goods and services and are often transferred to consumers. Examples include income tax, corporate tax, property tax, VAT, customs duty, and excise tax.

Economists also classify taxes according to their nature, incidence, base, and purpose. Taxes by nature may be proportional, progressive, or regressive. By incidence, they are direct or indirect. By base, they include income-based, consumption-based, and property-based taxes. By purpose, they include revenue taxes, regulatory taxes, and benefit taxes.

Principles Of Taxation

| Principle | Main Idea |

|---|---|

| Equity | Fairness in tax payments |

| Efficiency | Minimal economic distortion |

| Simplicity | Easy understanding and compliance |

| Certainty | Predictable obligations |

| Convenience | Easy methods of payment |

| Revenue Sufficiency | Adequate government revenue |

Types Of Taxes

| Type | Examples |

|---|---|

| Direct Taxes | Income tax, corporate tax, property tax |

| Indirect Taxes | VAT, customs duty, excise tax |

Worked Examples

Example 1

Scenario: A worker pays personal income tax based on the amount earned.

Explanation: This is a direct tax, and it reflects the principle of vertical equity because higher-income earners contribute more.

Example 2

Scenario: Consumers pay VAT when purchasing goods from shops.

Explanation: VAT is an indirect tax because its burden is passed on to consumers through the prices of goods and services.

Why This Topic Matters

Understanding taxation helps learners appreciate how governments finance public services and maintain economic stability. Knowledge of taxation also enables citizens and businesses to understand their financial responsibilities and contributions to national development.

Quick Practice

- Define taxation.

- State two examples of direct taxes.

- Explain the principle of certainty in taxation.

Summary

Taxation is a major source of government revenue and an essential tool of public finance. Tax systems are guided by principles such as equity, efficiency, simplicity, certainty, convenience, and revenue sufficiency. Taxes may be direct or indirect and can be classified according to their nature, incidence, base, and purpose. These classifications help governments design effective tax systems and promote economic development.

Access NaCCA-aligned Support Packs

Download your structured NaCCA-aligned Teacher Support Pack and Student Learning Pack, designed for clarity, practicality, and reliable teaching and learning.