Reasons For Holding Money And Roles Of Financial Institutions Explained for SHS 2 Economics (Semester 2, Week 7)

People do not hold money only for spending. They also keep money for emergencies and future investment opportunities, while financial institutions help ensure the smooth functioning of the economy.

What You Will Learn

- The three motives for holding money

- Examples of each motive

- The meaning of financial institutions

- The roles financial institutions perform in the economy

- Examples of financial institutions and their functions

Main Explanation

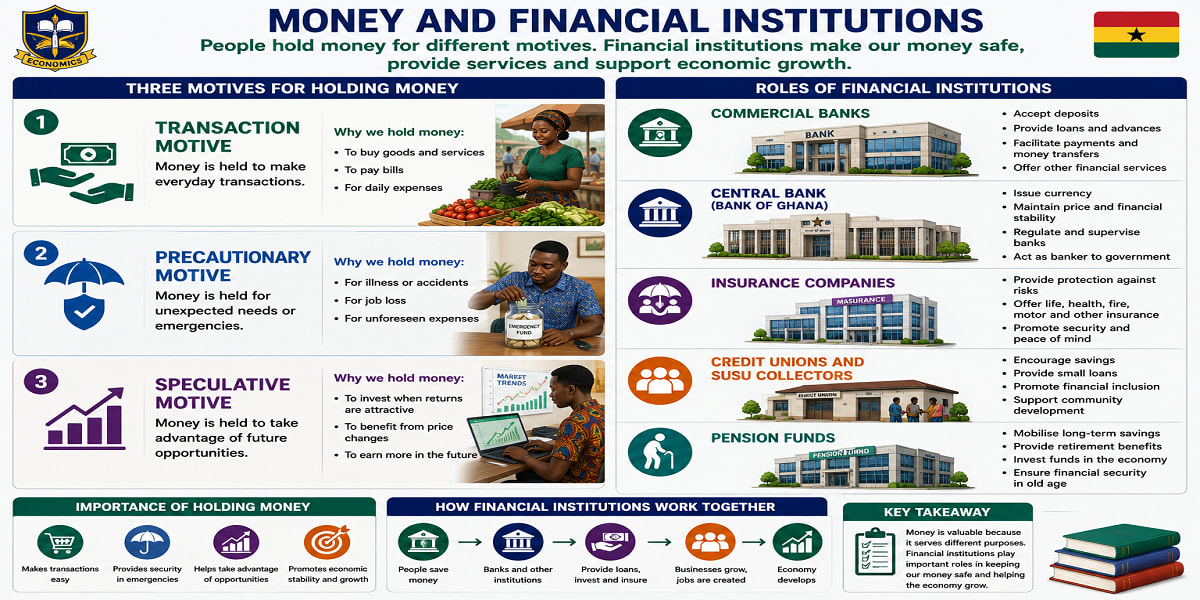

Individuals and businesses hold money for different purposes. Economists classify these reasons into transaction, precautionary, and speculative motives. These motives explain how money is used and why people maintain cash balances.

The transaction motive refers to holding money to meet daily expenses and planned purchases. Consumers use money to pay for food, transportation, rent, and utility bills, while businesses use it for salaries and supplies.

The precautionary motive involves keeping money for unexpected events such as illness, repairs, or periods of economic uncertainty. This reserve protects individuals and firms against unforeseen circumstances.

The speculative motive involves keeping funds available to exploit future investment opportunities. Investors may wait for favourable interest rates or lower asset prices before investing.

Financial institutions are essential to economic development because they facilitate the flow of money and provide important financial services. They connect savers with borrowers, facilitate payments, provide liquidity, and support economic growth.

Examples of financial institutions include commercial banks, central banks, investment banks, insurance companies, credit unions, and pension funds. Each institution performs specialised functions that contribute to the efficient functioning of the economy.

Motives For Holding Money

| Motive | Purpose | Illustration |

|---|---|---|

| Transaction | Daily expenses | Buying food and paying bills |

| Precautionary | Unexpected needs | Emergency medical expenses |

| Speculative | Future investments | Purchasing shares when prices decline |

Financial Institutions And Their Roles

| Institution | Main Role |

|---|---|

| Commercial Banks | Provide loans and deposits |

| Central Banks | Control money supply and inflation |

| Investment Banks | Raise capital for companies |

| Insurance Companies | Provide risk protection |

| Credit Unions | Offer member-based financial services |

| Pension Funds | Manage retirement savings |

Worked Examples

Example 1

Scenario: A family saves money to cover emergency hospital bills.

Explanation: This illustrates the precautionary motive because the money is kept to meet unexpected expenses.

Example 2

Scenario: A business obtains a loan from a commercial bank to expand its operations.

Explanation: Commercial banks act as intermediaries by providing credit to businesses and supporting economic growth.

Why This Topic Matters

Understanding the motives for holding money and the roles of financial institutions helps individuals manage resources effectively and appreciate how financial systems contribute to economic stability and development.

Quick Practice

- State the three motives for holding money.

- Explain the speculative motive.

- Identify three roles performed by financial institutions.

Summary

People hold money for transaction, precautionary, and speculative reasons. Financial institutions support economic activities through intermediation, payment services, liquidity provision, risk management, and savings mobilisation. These institutions play a central role in promoting economic growth and maintaining financial stability.

Access NaCCA-aligned Support Packs

Download your structured NaCCA-aligned Teacher Support Pack and Student Learning Pack, designed for clarity, practicality, and reliable teaching and learning.