Reasons For Holding Money And Roles Of Financial Institutions

Introduction

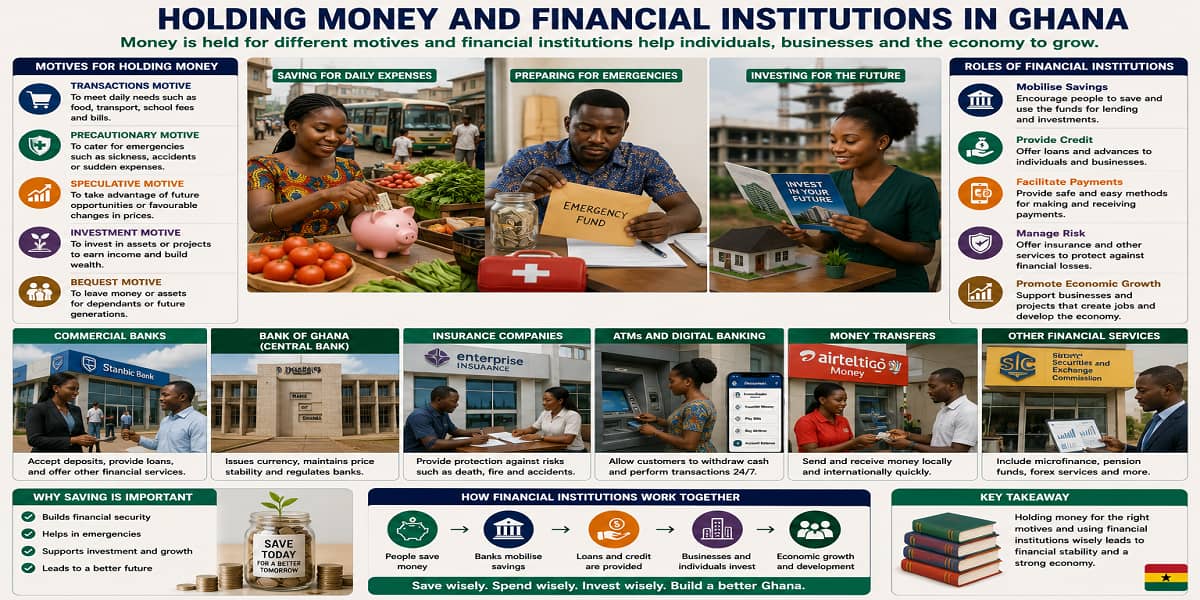

People and organisations hold money for different purposes, while financial institutions perform important functions that support economic growth and stability. Understanding the motives for holding money and the roles of financial institutions helps explain how resources are managed and how financial systems contribute to economic development.

Key Concepts

- Transaction Motive: Holding money to meet everyday expenses and immediate purchases.

- Precautionary Motive: Holding money to cater for unexpected expenses and emergencies.

- Speculative Motive: Holding money to take advantage of future investment opportunities.

- Financial Institutions: Organisations that facilitate the flow of money and provide financial services.

- Intermediation: The process by which financial institutions connect savers and borrowers.

- Liquidity: The availability of funds for immediate use.

- Financial Inclusion: Providing accessible financial services to different groups within society.

Explanation

Individuals and organisations hold money for three major reasons: transaction motive, precautionary motive, and speculative motive. These motives explain why people keep money rather than spending or investing all of it immediately.

Transaction Motive refers to holding money to meet daily expenses, business operations, and planned purchases. Individuals use money to pay for food, transportation, utility bills, and other necessities, while businesses maintain cash reserves for salaries and supplies.

Precautionary Motive refers to keeping money for unforeseen situations such as medical emergencies, home repairs, equipment breakdowns, or economic uncertainty. Businesses and individuals maintain reserves to protect themselves against unexpected events.

Speculative Motive involves holding money to take advantage of future investment opportunities and favourable market conditions. Investors may keep funds available to purchase assets when prices fall or when interest rates change.

Reasons For Holding Money

| Motive | Description | Examples |

|---|---|---|

| Transaction Motive | Meeting daily expenses and planned purchases | Paying rent and buying groceries |

| Precautionary Motive | Preparing for emergencies | Medical expenses and repairs |

| Speculative Motive | Taking advantage of investment opportunities | Buying stocks when prices fall |

Financial institutions play important roles in the economy by facilitating the movement of money, providing financial services, and supporting economic growth. They act as intermediaries between savers and borrowers and help allocate resources efficiently.

The major roles of financial institutions include intermediation, facilitating payments, providing liquidity, risk management, mobilising savings, promoting economic stability and growth, encouraging financial inclusion, and providing information. These functions contribute to the efficient operation of the economy.

Roles Of Financial Institutions

| Role | Description | Economic Importance |

|---|---|---|

| Intermediation | Connects savers and borrowers | Efficient allocation of resources |

| Facilitating Payments | Provides payment systems | Smooth economic transactions |

| Providing Liquidity | Offers short-term credit | Supports daily operations |

| Risk Management | Provides insurance and financial products | Reduces uncertainty |

| Mobilising Savings | Encourages savings and investment | Creates funds for development |

| Economic Stability And Growth | Supports business and monetary policy | Promotes development |

| Financial Inclusion | Provides accessible services | Reduces poverty |

| Information Provision | Supplies credit and market information | Improves decision-making |

Examples Of Financial Institutions And Their Roles

| Financial Institution | Role | Examples Of Activities |

|---|---|---|

| Commercial Banks | Provide loans and deposits | Money transfers and savings accounts |

| Central Banks | Implement monetary policy | Control inflation and manage reserves |

| Investment Banks | Raise capital | Issue stocks and bonds |

| Insurance Companies | Manage risks | Provide insurance products |

| Credit Unions | Serve members | Offer savings and loans |

| Pension Funds | Manage retirement savings | Invest contributions for future benefits |

Examples

Example 1

Problem: Explain why an individual keeps money for emergency medical expenses.

- Identify the purpose of holding the money.

- Determine whether the expense is expected or unexpected.

- Classify the motive.

Final Answer: This illustrates the precautionary motive because the money is reserved for unforeseen emergencies.

Example 2

Problem: State one role of commercial banks.

- Identify the institution.

- Determine its services.

- State the role performed.

Final Answer: Commercial banks provide loans and deposit accounts for individuals and businesses.

Application and Activities

- Discuss situations in which individuals hold money for different motives.

- Identify financial institutions operating within your community.

- Explain how banks and insurance companies contribute to economic growth.

- Compare the functions of commercial banks and central banks.

Practice Questions

- State the three motives for holding money.

- Explain the precautionary motive for holding money.

- Discuss four roles performed by financial institutions in an economy.

Summary

Money is held for transaction, precautionary, and speculative motives. These motives enable individuals and organisations to meet daily needs, prepare for emergencies, and exploit investment opportunities. Financial institutions perform vital roles such as intermediation, facilitating payments, providing liquidity, managing risks, mobilising savings, promoting economic growth, supporting financial inclusion, and providing information. Their activities contribute significantly to the efficient functioning of the economy.

Access NaCCA-aligned Support Packs

Download your structured NaCCA-aligned Teacher Support Pack and Student Learning Pack, designed for clarity, practicality, and reliable teaching and learning.