Principles, Types And Classification Of Taxation

Introduction

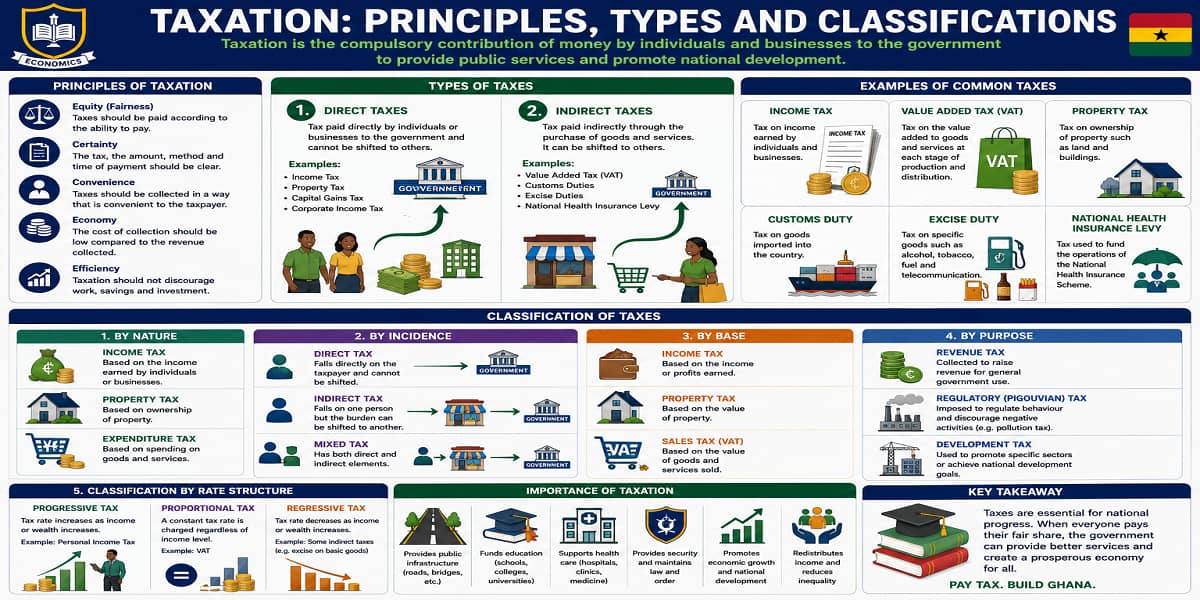

Taxation is an important aspect of public finance and economic policy. Governments impose taxes to generate revenue needed to provide public goods and services such as roads, healthcare, education, defence, and social welfare programmes. Taxation also contributes to resource distribution and economic stability.

Key Concepts

- Taxation: The process by which a government or its authorised authority imposes financial charges or levies on individuals, businesses, and other entities.

- Direct Tax: A tax whose burden falls directly on the taxpayer.

- Indirect Tax: A tax whose burden can be shifted to another party, usually consumers.

- Equity: The principle that taxpayers should contribute according to their ability to pay.

- Progressive Tax: A tax whose rate increases as taxable income increases.

- Proportional Tax: A tax with a constant rate regardless of income level.

- Regressive Tax: A tax whose burden decreases as income rises.

Explanation

Taxation refers to the process through which governments impose financial charges on individuals and organisations to raise revenue for public expenditure. Revenue generated from taxes is used to provide infrastructure, healthcare, education, defence, and social welfare services. Taxation plays an important role in maintaining economic stability and supporting development.

The principles of taxation guide the design and administration of tax systems. These principles include equity, efficiency, simplicity, certainty, convenience, and revenue sufficiency. Equity consists of horizontal equity, where taxpayers with similar ability to pay should contribute similar amounts, and vertical equity, where those with greater ability to pay contribute more.

Principles Of Taxation

| Principle | Description | Importance |

|---|---|---|

| Equity | Taxes are based on ability to pay | Promotes fairness |

| Efficiency | Minimises economic distortion | Encourages productivity |

| Simplicity | Easy to understand and comply with | Reduces administrative costs |

| Certainty | Taxpayers know their obligations | Promotes financial planning |

| Convenience | Taxes are paid at suitable times and methods | Improves compliance |

| Revenue Sufficiency | Generates adequate revenue | Supports government expenditure |

Taxes are broadly divided into direct and indirect taxes. Direct taxes are imposed directly on individuals and businesses and include income tax, corporate tax, wealth tax, and property tax. Indirect taxes are imposed on goods and services and include sales tax, Value Added Tax (VAT), excise tax, customs duty, and service tax.

Types Of Taxes

| Type Of Tax | Examples | Characteristics |

|---|---|---|

| Direct Taxes | Income tax, corporate tax, property tax | Paid directly by taxpayers |

| Indirect Taxes | VAT, customs duty, excise tax | Burden can be transferred to consumers |

Taxes may also be classified according to their nature, incidence, base, and purpose. By nature, taxes may be proportional, progressive, or regressive. By incidence, they are classified as direct or indirect taxes. By base, they may be income-based, consumption-based, or property-based taxes. By purpose, they may be revenue taxes, regulatory taxes, or benefit taxes.

Classification Of Taxes By Nature

| Classification | Description | Example |

|---|---|---|

| Proportional Tax | Constant tax rate | Flat tax rate |

| Progressive Tax | Tax rate rises with income | Graduated income tax |

| Regressive Tax | Tax burden falls as income rises | Sales tax |

Classification Of Taxes By Base And Purpose

| Category | Types | Examples |

|---|---|---|

| By Base | Income-based, consumption-based, property-based | Income tax, VAT, property tax |

| By Purpose | Revenue taxes, regulatory taxes, benefit taxes | Income tax, carbon tax, fuel tax |

Examples

Example 1

Problem: Identify the type and classification of Value Added Tax.

- Determine whether VAT is direct or indirect.

- Identify its nature.

- State an example of its application.

Final Answer: VAT is an indirect tax and is often regarded as regressive because it may take a larger proportion of income from low-income earners.

Example 2

Problem: Explain why income tax reflects the principle of vertical equity.

- Identify the principle involved.

- Consider taxpayers with different income levels.

- Determine how tax rates are applied.

Final Answer: Income tax reflects vertical equity because individuals with higher incomes pay higher tax rates.

Application and Activities

- Identify examples of direct and indirect taxes in Ghana.

- Discuss the importance of taxation in providing public services.

- Classify selected taxes according to their nature and purpose.

- Examine how taxation promotes economic stability.

Practice Questions

- Define taxation.

- Differentiate between direct taxes and indirect taxes.

- Explain three principles of taxation.

Summary

Taxation is the process through which governments impose financial charges to generate revenue for public expenditure. The principles of taxation include equity, efficiency, simplicity, certainty, convenience, and revenue sufficiency. Taxes are classified into direct and indirect taxes and may further be classified according to their nature, incidence, base, and purpose. Taxation is essential for economic development and public finance.

Access NaCCA-aligned Support Packs

Download your structured NaCCA-aligned Teacher Support Pack and Student Learning Pack, designed for clarity, practicality, and reliable teaching and learning.